Flow Batteries

Published: May 11, 2026

The complete climate deeptech commercialization map. 31 companies across vanadium, organic, zinc-bromine, iron, and emerging chemistries, from university spinouts to GWh-scale manufacturers.

A Brief History of Flow Batteries

The idea of storing energy in flowing liquids is older than most people realize. The first patent for a battery using liquid electrolytes pumped through a cell was filed in France in 1879. But the concept sat largely dormant until the mid-twentieth century, when German researchers began experimenting with electrochemical systems that separated energy storage from power delivery, a distinction that would become the defining feature of flow battery architecture.

The modern era of flow batteries began at NASA's Lewis Research Center in 1974, where engineers developed an iron-chromium system for space and terrestrial energy storage. NASA's work proved the core principle: by storing energy in liquid electrolytes held in external tanks, you could scale energy capacity independently of power output simply by adding more fluid. That decoupling remains the fundamental advantage that flow batteries hold over every solid-state chemistry today.

The real breakthrough came in the 1980s at the University of New South Wales in Australia. Maria Skyllas-Kazacos and her team developed the all-vanadium redox flow battery, using vanadium in both the positive and negative electrolytes. The elegance of the single-element approach solved a problem that had plagued earlier dual-element systems: cross-contamination between the two electrolytes. If vanadium ions crossed the membrane, they simply joined the other vanadium solution rather than degrading it. This meant vanadium flow batteries could theoretically cycle indefinitely without capacity loss, a claim that no lithium-ion battery can make.

Through the 1990s and 2000s, several companies attempted to commercialize flow batteries (notably Regenesys in the UK (sodium-bromine polysulphide) and VRB Power Systems in Canada) but most struggled with manufacturing cost and market timing. The grid-scale storage market simply didn't exist yet. It wasn't until the 2010s, when renewable penetration began creating genuine duration problems on the grid, that the economics started to shift. The emergence of all-iron chemistries (ESS Inc, founded 2011), organic electrolytes (CMBlu, also 2011), and aggressive Chinese state-backed deployment (Dalian Rongke Power's GWh-scale station) transformed flow batteries from a niche research topic into a real commercial category with over $2 billion in cumulative investment.

How a Flow Battery Works

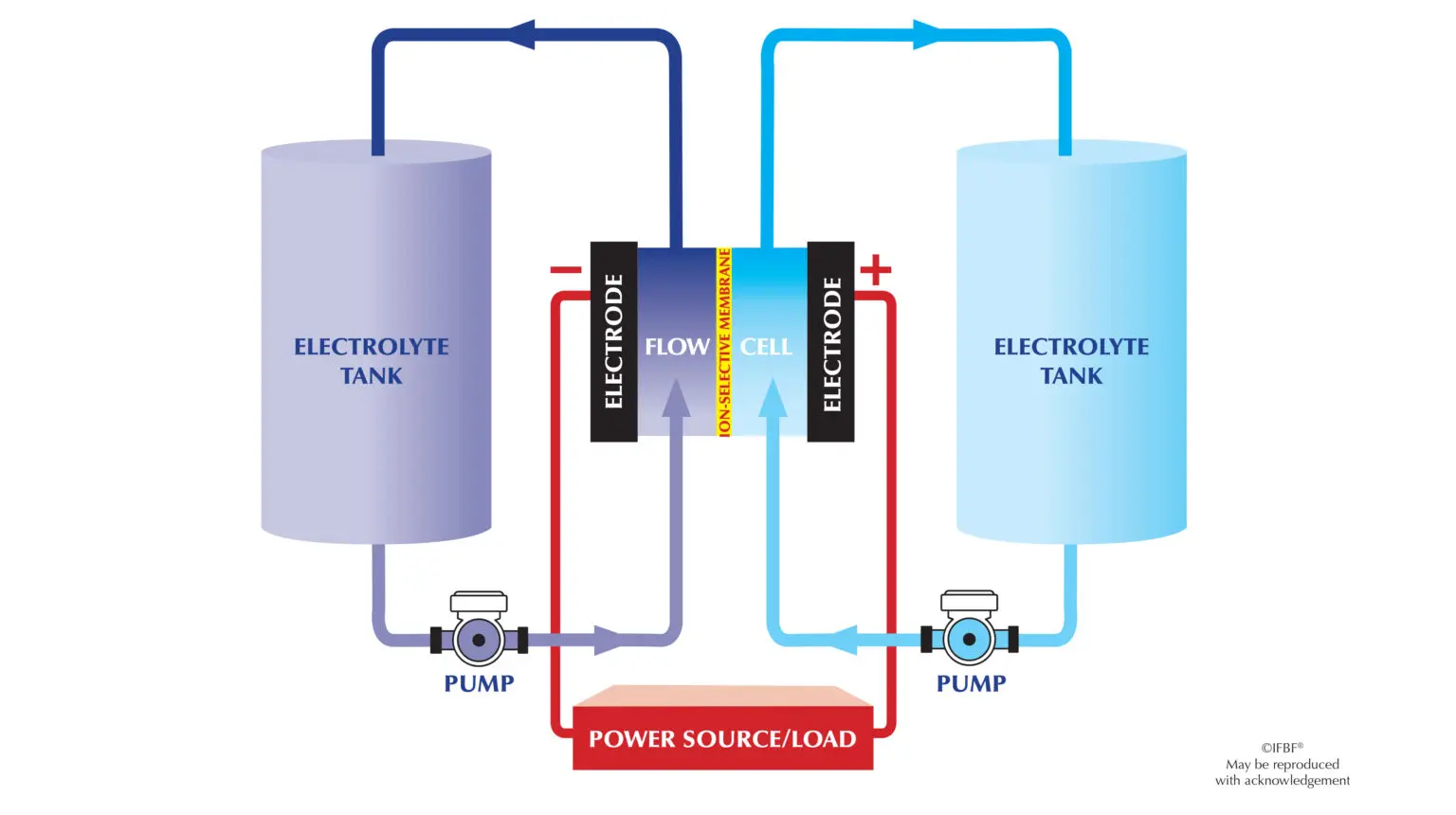

A flow battery stores energy in liquid electrolytes (typically water-based solutions containing dissolved active materials) held in external tanks. When the battery charges or discharges, pumps circulate these liquids through a central cell stack, where electrochemical reactions convert between electrical and chemical energy. The two electrolyte solutions (called the anolyte and catholyte) flow on opposite sides of a membrane that allows ions to pass through while keeping the solutions separate.

The cell stack is where the power conversion happens. Inside, electrode surfaces provide the reaction sites, and a thin ion-exchange membrane sits between them. During discharge, one electrolyte is oxidized (loses electrons) while the other is reduced (gains electrons), generating an electric current. During charging, the process reverses. The membrane's job is to let charge-balancing ions through while preventing the two electrolyte solutions from mixing.

What makes this architecture fundamentally different from a lithium-ion battery or any solid-state system is the separation of power and energy. The cell stack determines how much power (kW) the system can deliver. Add more cells, get more power. The tanks determine how much energy (kWh) the system can store. Add more electrolyte, get more duration. This means doubling the storage duration of a flow battery does not require doubling the cost. You just need bigger tanks and more fluid, which are cheap relative to the electrochemical components. For applications requiring 8, 12, or even 100+ hours of storage, this scaling relationship gives flow batteries a structural cost advantage over lithium-ion, where energy and power are locked together in every cell.

Most flow battery electrolytes are water-based, which makes them inherently non-flammable, a meaningful safety advantage over lithium-ion systems, particularly for siting near residential areas, inside buildings, or at critical infrastructure. The electrolytes also don't degrade the way solid electrode materials do, which is why many flow battery manufacturers quote 20- to 30-year lifespans with minimal capacity fade.

Flow batteries also have near-zero self-discharge. Only the small volume of electrolyte sitting inside the cell stack is subject to parasitic reactions when the system is idle; the bulk volume in the external tanks is completely unaffected. In practice, standby losses are typically less than 1% of total stored energy, a significant advantage for seasonal or multi-day storage applications. They also have no memory effect, meaning they can be discharged to 0% and recharged to 100% without any degradation in capacity.

Despite the presence of pumps and tanks, flow batteries respond fast. The electrolyte already inside the stack delivers power within milliseconds, bridging the brief startup time for the pumps. This means a single flow battery system can provide both long-duration energy shifting and rapid grid services like frequency regulation and voltage support simultaneously, sometimes referred to as "stacked services."

Chemistry Types

Not all flow batteries are created equal. The choice of active materials in the electrolyte determines cost, performance, supply chain risk, and application fit. Here are the major chemistry families competing in the market today.

All-Vanadium (VRFB)

Uses vanadium in both electrolytes, eliminating cross-contamination risk. The most commercially deployed flow battery chemistry with GWh-scale installations in China and deployments in 20+ countries. Electrolyte is fully recyclable and retains value indefinitely. Downside: vanadium prices are volatile and supply is geographically concentrated in China, Russia, and South Africa. Current installed cost around $384/kWh for large systems.

Zinc-Bromine

A hybrid flow battery where zinc is plated as a solid on the anode during charging and dissolved back during discharge. Only one electrolyte flows, simplifying system design. Some designs (Primus Power) eliminate the membrane entirely, reducing cost and maintenance. Trade-off: zinc dendrite formation can limit cycle life, and bromine is corrosive. Well-suited to commercial and industrial applications requiring 4–8 hours of storage.

Iron-Based (All-Iron & Iron-Chromium)

Uses earth-abundant iron (and sometimes chromium) as active materials, promising the lowest raw material costs of any flow battery chemistry. NASA originally developed iron-chromium in the 1970s. All-iron variants (ESS Inc) use iron, salt, and water only. The challenge has been lower energy density and slower reaction kinetics compared to vanadium, requiring larger systems for equivalent output. Iron-chromium (Redox One) benefits from decades of research but remains less commercially mature than vanadium.

Organic (Aqueous)

Replaces metal-based active materials with carbon-based organic molecules (typically quinones or similar compounds) dissolved in water. Organic molecules can be synthesized from abundant feedstocks, avoiding the supply chain risks of vanadium and other metals. CMBlu, Quino Energy, Jena Flow Batteries, KEMIWATT, and others are developing variants. The technology is less mature than vanadium but promises dramatically lower material costs. CMBlu's SolidFlow variant stores active material in a solid carbon compound rather than dissolving it, enabling higher energy density.

Hydrogen-Bromine & Hydrogen-Iron

Uses hydrogen gas on one side of the cell and a halide or metal-ion solution on the other. Elestor developed a hydrogen-bromine system but is pivoting to hydrogen-iron (H2Fe) due to geopolitical supply concerns around bromine. These chemistries can achieve high power density but add complexity through hydrogen handling. Still largely pre-commercial.

Acid-Base (Saltwater) & Other

AquaBattery's system splits salt water into acid and base streams to store energy, completely non-toxic and fully recyclable. Halide Energy is developing a copper-based flow battery (copper is roughly 10x cheaper than vanadium). Lockheed Martin's GridStar Flow uses a proprietary undisclosed chemistry. These niche approaches trade proven performance for potential cost or safety advantages, and most are still at pilot stage.

Use Cases

Flow batteries occupy a specific niche in the energy storage landscape: applications where long duration (6+ hours), high cycle life, and safety matter more than energy density or fast response. Here's where they're being deployed today and where the demand pipeline is building.

Utility-Scale Grid Storage

The primary market. Utilities need 8–12+ hour storage to shift renewable generation from afternoon solar peaks to evening demand. Flow batteries' ability to scale duration cheaply makes them more economical than lithium-ion beyond 6 hours. Dalian Rongke's 800 MWh station is the benchmark. Invinity's 16.7 GWh UK pipeline targets this segment.

Renewables Integration

Co-located with wind and solar farms to smooth intermittent output and provide firm, dispatchable power. The non-degrading electrolyte and 20+ year lifespan align with the lifecycle of renewable assets. VRB Energy and Largo/Storion are building supply chains specifically for this pairing.

Data Centers

Hyperscale data centers need 24/7 backup power and increasingly want to match load with clean energy around the clock. Flow batteries offer non-flammable, long-duration storage that can sit inside or adjacent to facilities. CMBlu is targeting US hyperscalers; XL Batteries has its first data center deployment with Prometheus Hyperscale; TerraFlow has a 4 GW+ data center pipeline.

Microgrids & Remote Power

Islands, remote communities, and military bases need reliable off-grid power. Flow batteries' safety profile (no fire risk, no toxic gas emissions) and long lifespan reduce the logistics burden of battery replacement in hard-to-reach locations. CellCube has 130+ installations globally including military sites.

Industrial & Commercial

Peak shaving, demand charge management, and backup power for commercial facilities. Volterion targets EV charging infrastructure and industrial grid stabilization. StorEn Technologies focuses on compact systems for commercial and residential segments.

Ports, Airports & Critical Infrastructure

Airport electrification, port shore power, and other infrastructure that demands both high reliability and zero-emission operation. KEMIWATT recently secured investment from maritime terminal operators Stolt Ventures and Impact Océan Capital to deploy at ports. Bryte Batteries and TerraFlow are developing long-duration UPS concepts for critical loads.

Policy Landscape

Flow battery deployment is heavily shaped by energy storage policy, both incentives that that make projects financeable and regulations that create structural demand for long-duration storage. The policy environment has shifted meaningfully in the last two years.

United States: Inflation Reduction Act

The IRA provides a 30% Investment Tax Credit (ITC) for standalone energy storage, rising to 50% or more with domestic content and energy community bonuses. This is the single most important policy driver for flow battery projects in North America. Critically, the ITC applies to standalone storage for the first time (previous rules required co-location with solar), unlocking flow batteries for grid-scale applications. The IRA also includes production tax credits for domestic manufacturing of battery components, which companies like Storion Energy and VRB Energy are positioning to capture.

United Kingdom: Cap & Floor Scheme

The UK's Long Duration Electricity Storage (LDES) Cap & Floor mechanism, managed by Ofgem, provides revenue certainty by guaranteeing a minimum return (the floor) while capping upside. Invinity Energy Systems has built a 16.7 GWh pipeline specifically around this scheme. The Cap & Floor model is significant because it reduces the bankability problem: lenders can underwrite projects against a guaranteed revenue floor rather than relying on volatile energy market prices.

European Union

The EU Clean Industrial Deal (2025) sets a target of 200 GW of energy storage by 2030, up from roughly 25 GW today. The European Grids Package mandates that transmission system operators integrate storage into grid planning. Flow Batteries Europe (FBE), the industry association, has been advocating for technology-neutral storage procurement and recognition of flow batteries' recycling advantages. The EU Batteries Regulation will require carbon footprint declarations for industrial batteries from 2030, which could advantage flow batteries (especially organic and iron-based chemistries) over lithium-ion given their lower lifecycle emissions and fully recyclable electrolytes.

Asia-Pacific

China remains the largest market by deployed capacity, driven by state-backed mandates for renewable-plus-storage projects. South Korea's K-RE100 program is creating demand for industrial storage. Japan's Ministry of Economy, Trade and Industry has funded VRFB development through Sumitomo Electric since the early 2000s. The Asia-Pacific policy environment favors incumbents (Rongke, Sumitomo, H2 Inc) with established manufacturing and government relationships.

Market Snapshot

Global Flow Battery Market

Projected growth, 2024 to 2030

Source: MarketsandMarkets (Dec 2024). Other estimates (Grand View Research) project higher values depending on scope.

Companies by Chemistry

Distribution across 31 mapped companies

Companies by Commercial Status

Maturity distribution across 31 companies

Companies by Region

Geographic distribution across 31 companies

Note: Asia count reflects companies headquartered in the region. Chinese state-backed players (Rongke) dominate deployed capacity despite fewer mapped companies.

Commercialization Progress

Flow batteries are no longer a science project. The sector has reached an inflection point: over $2 billion in cumulative venture and project funding, GWh-scale deployments live in China, and the first organic chemistry company (CMBlu) just hit unicorn status. The 31 companies mapped here span six-plus chemistry families, 15 countries, and every stage from university spinout to publicly traded manufacturer. This is a real market now.

But the commercialization gap remains enormous. The fundamental challenge hasn't changed: flow batteries are competing on duration (8–12+ hours) where lithium-ion can't follow, but they're still losing on upfront cost where lithium-ion dominates. Vanadium remains the most mature chemistry, but vanadium's price volatility and geographic concentration create supply chain risk that makes utility procurement teams nervous. The organic chemistry wave, led by CMBlu, Quino Energy, KEMIWATT, and XL Batteries, promises to solve the materials problem by using abundant carbon-based molecules, but none have proven manufacturing scale yet. And there's a policy dependency: the US IRA's investment tax credit and the UK's Cap and Floor Scheme are driving project pipelines, but policy-dependent demand is fragile demand.

The companies positioned to win are the ones solving for bankability, not just technology performance. Look at where commercial traction is actually happening. Dalian Rongke Power has over 2 GWh deployed because it has state-backed offtake and integrated manufacturing. Invinity is building a 16.7 GWh pipeline through the UK government's Cap and Floor Scheme, converting policy into contracted revenue. Storion Energy is attacking the cost barrier directly with an electrolyte leasing model that turns vanadium (the single largest cost component) from CapEx into OpEx. And CMBlu just raised €50M at a billion-dollar valuation by targeting US hyperscaler data centers, the one customer segment with both the budget and the duration needs to justify flow battery premium pricing.

The companies struggling are the ones with great technology and no commercial strategy. ESS Inc, despite pioneering iron flow chemistry and having a $9.9M Air Force contract, posted just $1.6M in revenue for all of 2025 and is publicly warning about its ability to continue operations, though its acquisition of VoltStorage's iron-salt battery IP in early 2026 could strengthen its technology portfolio. Technology differentiation alone doesn't build a business.

The DOE's Long-Duration Storage Shot has set a target of $0.05/kWh levelized cost of storage (LCOS) for 10+ hour systems. Current projections put vanadium systems at around $0.16/kWh LCOS by 2030, still more than 3x the target. Organic and iron chemistries may get closer, but no one is there yet. The market, projected to grow from approximately $1.4 billion in 2026 to $3.9 billion by 2031 at a 23% CAGR, will reward the companies that solve for cost, bankability, and supply chain before they try to scale. That's the commercialization playbook that separates the companies that survive the valley of death from the ones that don't.

Company Database

Click any column header to sort. Use filters to narrow results.

| Company | HQ | Founded | Stage | Raised | Chemistry | Status |

|---|

Building climate deeptech?

endré is the GTM and commercialization partner for climate deeptech startups. From pre-seed to Series B. 4 unicorns, 12 exits, $3B+ VC raised.

Get in Touch